The Illusion of Predictability

25 June 2025

My last post on X (or a tweet, or whatever Elon prefers to call it these days) was back in February 2024. At the time, I shared my critique of the ‘Bitcoin Power Law Model’. That attempt failed miserably, something I probably should have expected.

People quickly accused me of not knowing what I was talking about and told me I should approach the issue like a physicist. After all, explaining financial market dynamics is apparently not something an econometrician like me should do.

Tim Stolte, MSc in Quantitative Finance

Since then, I’ve stepped away from these types of discussions on social media. They’re no longer about who is right, but about who can strike the best balance between bold optimism and scientific reasoning. Lofty price predictions often rely on appeals to authority, and somewhere between all the academic titles, the actual arguments tend to get lost.

In fact, we might as well talk about “argument” in the singular, because most of the time it comes down to one: the R-squared. This is a statistical measure that indicates how much of the variation in price a model can explain. Often, an R-squared above 95 percent is presented, followed by the conclusion that the model can predict prices almost perfectly. But is 95 percent really that high? Let’s take a closer look.

Lies, Damned Lies and Statistics

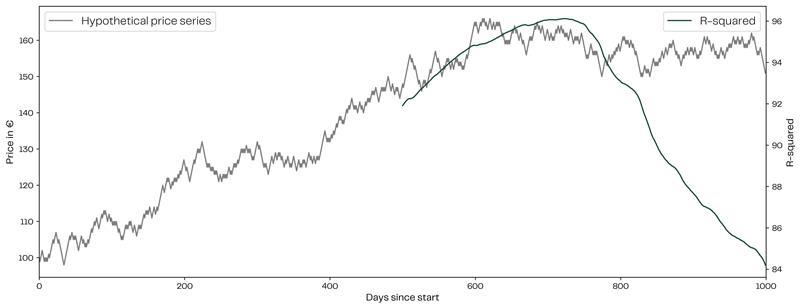

Imagine a hypothetical price series. It starts at €100 and moves up or down by €1 each day, with a 50 percent chance either way. A coin toss, essentially. We know in advance that this kind of price movement is impossible to explain or predict.

Figure 1: a random price series (left) and the R-squared of the linear regression of the price series against the number of days since the start.

Still, let’s give it a try. On day 500, we run a regression of the price on the number of days that have passed. By chance, the first 500 days show a slight upward trend. As a result, the R-squared comes out to 92 percent. By day 700, the trend continues, and the R-squared reaches 96 percent.

Here’s the issue. If we were to conclude based on that 96 percent that the price is predictable, we’d be wrong. In the days that follow, the trend flattens out, a direct result of the underlying randomness of the series.

Even for an asset that is entirely unpredictable, we can still end up with a very high R-squared. In other words, a high R-squared tells us very little about whether a model can actually predict future prices.

This doesn’t mean that bitcoin is equally unpredictable. Many factors and events influence its market value. But if we can already be misled by a model in a fully random situation, then the potential for misinterpretation is even greater in a market that contains some degree of predictability.

Made for the Stage

We need to be cautious with long-term price models and forecasts. Not just because most people don’t know how to spell them, but because they often lead to bruised egos and personal attacks on social media. More importantly, they can result in misplaced confidence and significant financial loss.

Most of these models have already outlived their purpose. Yes, traditional institutions may need a forecast to justify their entry into crypto markets, but a rough estimate based on historical growth is usually enough. They may reference something like the Stock-to-Flow Model once in a hundred-slide deck and never look at it again.

As asset managers, we don’t use these types of models either. Our investment decisions aren’t based on price forecasts, because they almost always lead to underperformance or avoidable risk. Nearly every model assumes that bitcoin’s price rises indefinitely. In the long run, this would imply a constant crypto allocation — which we would advocate anyway based on fundamentals.

Number Go Up

The largest group engaged in long-term bitcoin price predictions are retail investors, who enjoy projecting their future wealth based on current holdings. There’s nothing wrong with that. Conviction is an important part of any investment decision. But ideally, that conviction is based on well-reasoned assumptions, not pseudoscientific claims.

At some point, someone will say, “All models are wrong, but some are useful.” In this context, I completely disagree. Not with the second part, but with the first.

In fact, most price models are technically correct. They describe bitcoin’s historical price movements remarkably well. What people choose to do with that insight is a different matter.

It’s not the models that are flawed, but the conclusions people draw from them. The predictive power of these models is actually quite limited. And that conclusion, at least, is a useful one.

Our website uses cookies

We use cookies to personalize content and advertisements, to offer social media features and to analyze our website’s traffic. We’ll also share information about your usage with our partners for social media, advertising and analysis. These partners can combine this data with data you’ve already provided to them, or that they’ve collected based on your use of their services.