« Alors on danse » - The Greatest Bull Run in History?

23 July 2025

We’re halfway through the year. A good moment to take stock. What did the first half of 2025 bring — and what might the second half hold?

As asset managers, our job is to look ahead. We do this by piecing together various fragments of information like a jigsaw puzzle, in search of an overarching market picture.

In this piece, I focus on macroeconomic developments in the US and Europe that currently influence risk markets like equities and crypto — and I share my expectations for the coming six months.

Let’s start with the factor that has triggered some of the most notable price moves in recent months.

Import tariffs: the elephant in the room

Trump is a fan — he loves to impose them, or at least threaten to. But by now it’s also clear that he’s perfectly willing to shelve tariffs if equity markets start feeling the pressure.

That’s exactly what we saw on April 9, when Trump paused his tariff plan for 90 days after a notable drop in equity markets. As soon as the pause was announced, those markets rebounded just as sharply as they had fallen. Something Trump surely didn’t miss.

Since then, his policy has been classically “Trumpian.” Tariffs on various products and countries have been imposed, raised, delayed, or reversed — in such a way that simply keeping track has become a full-time job.

My expectation is that import tariffs will remain in some form, but not at a level that meaningfully disrupts international trade or risk markets.

Monetary policy on hold

The two most important players here are the Federal Reserve (FED), and to a lesser extent the European Central Bank (ECB). The FED has a dual mandate: maximum employment and price stability. The ECB focuses solely on price stability.

On employment, we can be brief. Unemployment is low, with no signs suggesting it might rise. In fact, a key monthly gauge of newly created jobs in the US economy (Non-Farm Payrolls) has been exceeding analyst expectations for several months now.

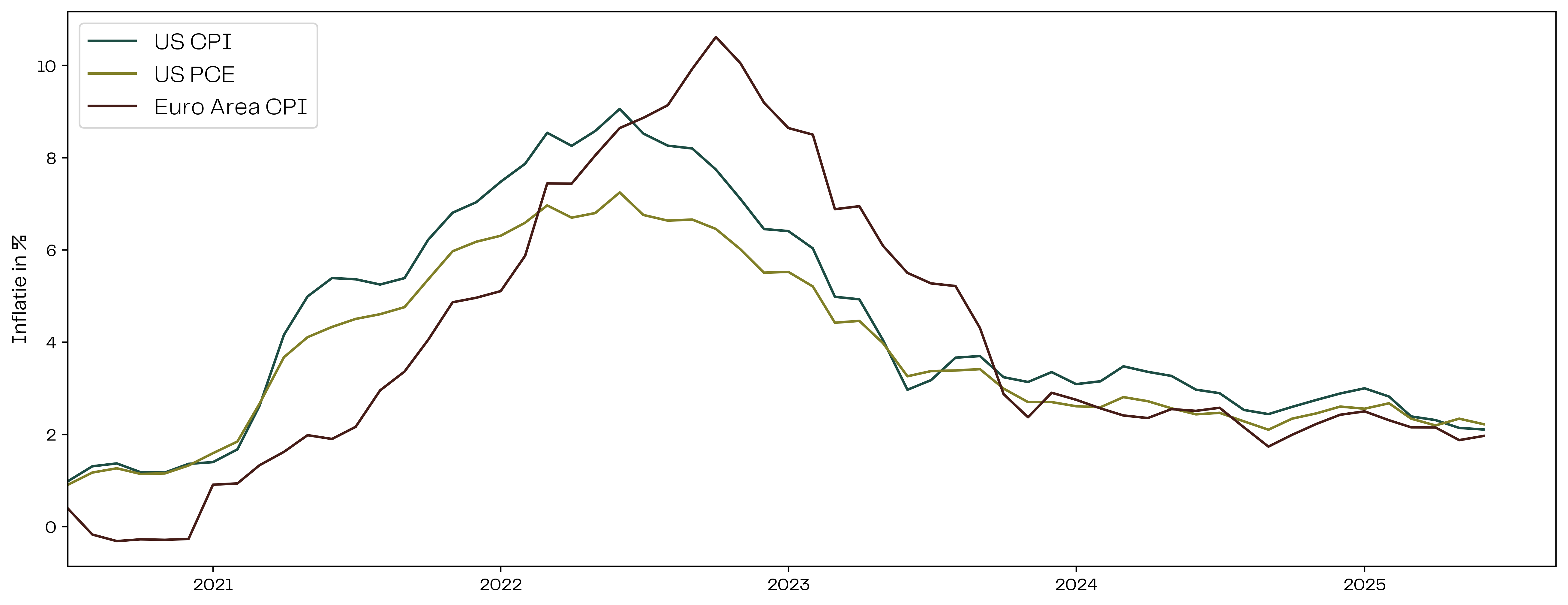

Price stability is more complex. The two main inflation metrics for consumers are CPI (consumer price index) and PCE (personal consumption expenditures). In the eurozone, CPI is the primary measure — in the United States, both are closely monitored.

Figure 1: Consumer price inflation (CPI) and core inflation (PCE) for the United States, compared to eurozone CPI.

As the chart above shows, inflation has been stabilizing for some time now, heading toward the 2% target. That’s particularly good news for the FED, as it opens the door to potential rate cuts — which is expected to benefit risk markets.

At the same time, we see the FED taking a more cautious stance than the ECB. The main reason is that Trump’s tariff policy injects uncertainty on the inflation front.

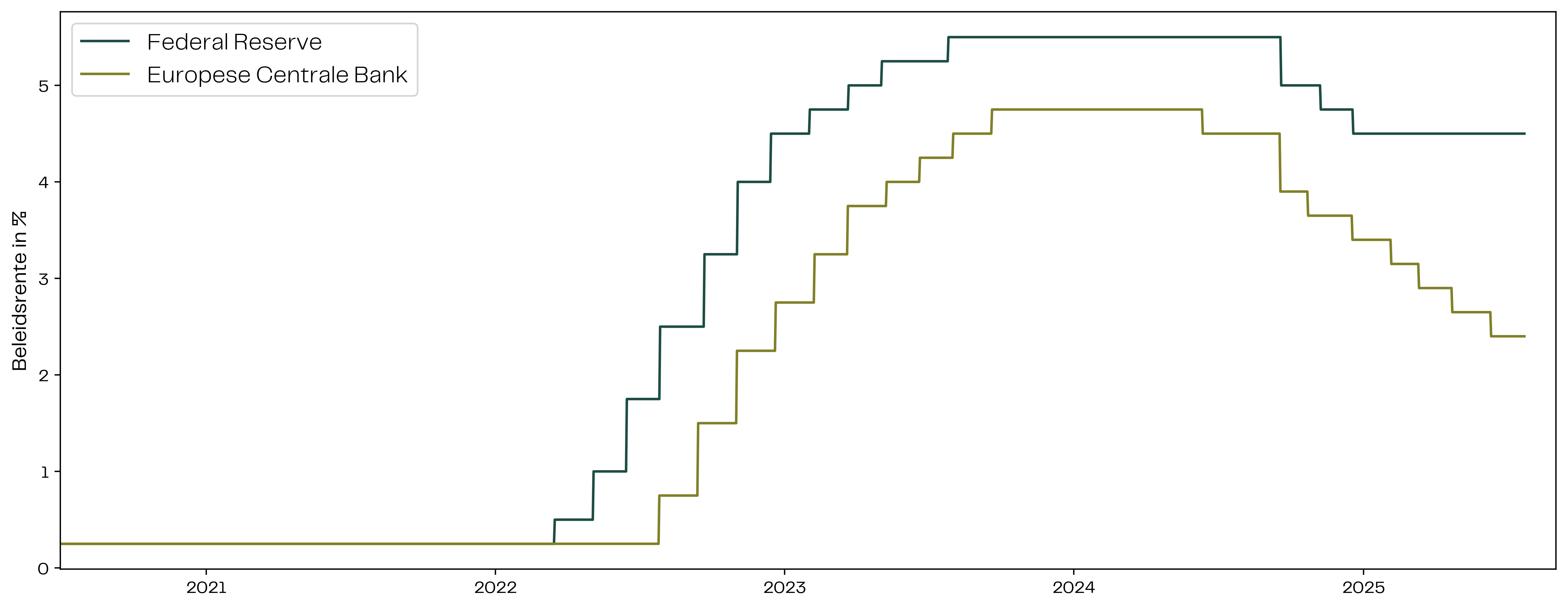

Figuur 2: Policy rates of the US Federal Reserve and the European Central Bank, 2020–2025.

The FED is holding off — visibly to Trump’s frustration. In recent weeks he publicly aired his displeasure with Chair Powell, issuing sharp criticism and thinly veiled threats. Then, on July 16, a sudden reversal: according to Trump, firing Powell was now “extremely unlikely.” A textbook example of Trumpian governance.

In any case, Powell’s term ends early next year. It’s likely Trump will appoint an unapologetic dove as his successor. That makes rate cuts a matter of time — and that’s generally positive for risk assets.

Governments return to growth

In my previous article, I wrote about how DOGE had only made symbolic spending cuts, while the “One Big Beautiful Bill” pushed the deficit further into the red. I also predicted continued upside in bitcoin and risk markets. And that’s exactly what happened. Both major US stock indices and bitcoin have since reached new all-time highs.

In the US, a new law has now been passed that grants every child born between 2025 and 2028 an investment account funded with a one-time $1,000 contribution. This money comes from the Treasury and will be invested in a low-cost index fund.

The US government has offered several justifications for this policy — some more convincing than others. But the cynic in me sees it as a signal: they’ll do whatever it takes to keep equity markets rising. An interesting sidenote: Hillary Clinton originally proposed this idea back in 2008.

On the European side of the Atlantic, we’re seeing a similar pattern. The NATO spending norm is rising to 5%, and Germany has lifted its so-called “debt brake.” This gives the German government more room to stimulate its struggling economy. Not every EU country will be able to match that pace, but the growth momentum in Europe is unmistakably turning upward.

The market wants to go higher

That’s the conclusion we’re left with after assembling all the puzzle pieces. It also spells bad news for the dollar, muted prospects for US Treasuries, and good news for gold, equities, and crypto.

The million-dollar question no one can answer with certainty is: how long can this go on?

My view? As long as the music plays, more chairs will be added — and the party will only grow more exuberant. So we keep dancing.

Our website uses cookies

We use cookies to personalize content and advertisements, to offer social media features and to analyze our website’s traffic. We’ll also share information about your usage with our partners for social media, advertising and analysis. These partners can combine this data with data you’ve already provided to them, or that they’ve collected based on your use of their services.