"Prices are declining because the biggest reason for rising prices is now behind us.”

2 October 2025

Monthly: September 2025

Summary

September once again brought weak U.S. labor market data, though investors initially viewed this as a positive sign: the Federal Reserve would likely continue with accommodative policy. Equities and crypto rallied briefly, until the latter corrected by more than 10% following the rate cut, driven in part by liquidations. Still, there are few signs that the market has reached a definitive top, allowing crypto investors to enter the final quarter with confidence.

History does not always repeat itself

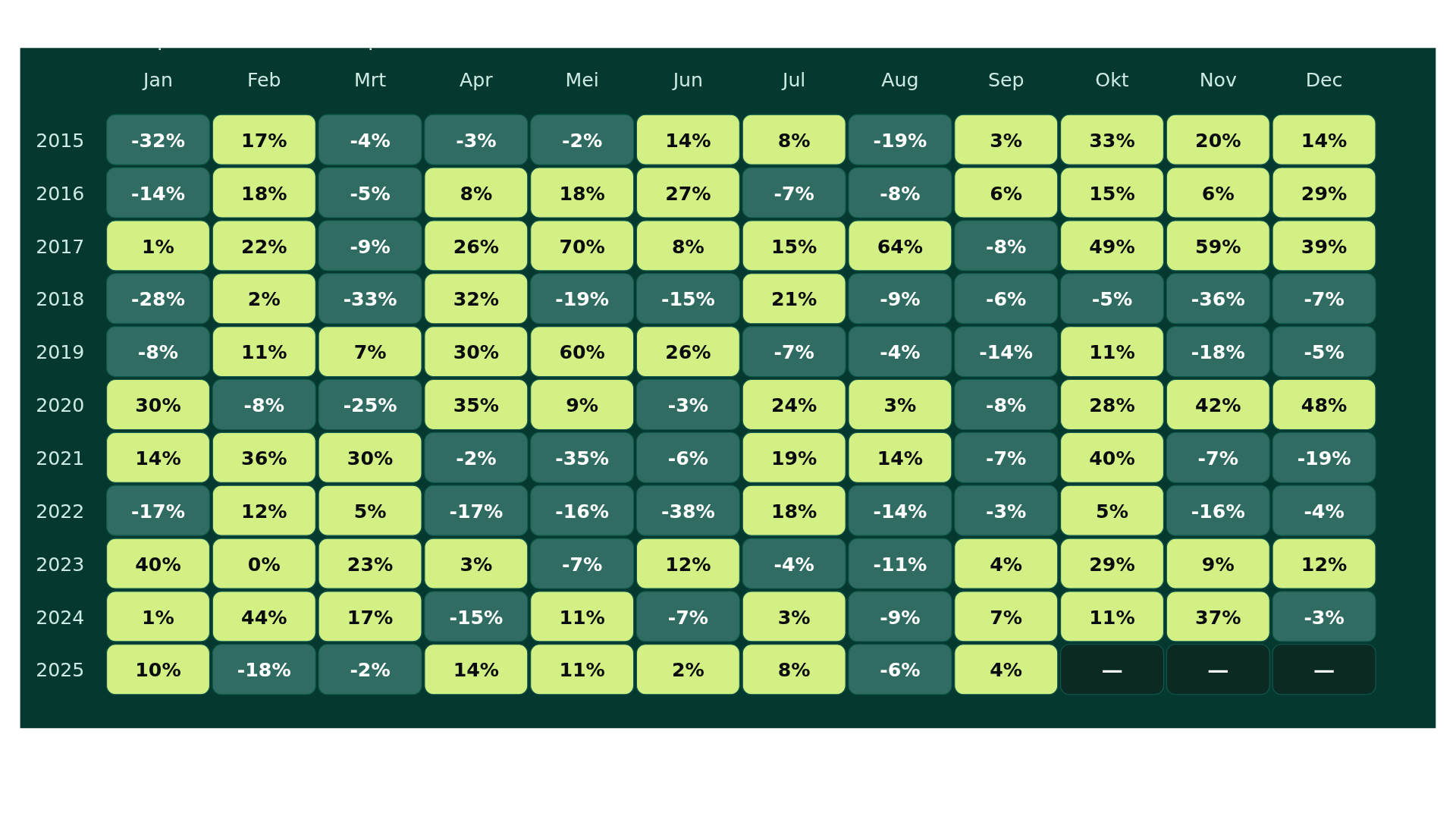

Historically, September is the weakest of the twelve months, with an average bitcoin return of -3.2% since 2010. Yet markets paid little attention to that pattern this year. Bitcoin gained 5.3%, lifting the broader crypto market by about 3%.

Figure 1: Historic bitcoin perfomance

It seems we do not always need to fear the supposed seasonality of crypto markets. And with the final quarter ahead, it is worth noting that Q4, with an average return of 25.8%, has historically been by far the strongest. Will we see another powerful year-end rally, or is the so-called “crypto summer” in autumn finally over?

Working under pressure

September picked up where August left off. U.S. labor market reports once again revealed grim numbers, showing that 911,000 fewer jobs were added to the economy over the past year than initially expected. This marked the largest revision on record.

On top of these hard numbers, the softer data also painted a bleak picture. The Purchasing Managers’ Index (PMI), a survey of corporate managers that tracks business activity, still pointed to a shrinking industrial workforce. This only covers part of the U.S. labor market, but it is often the first group to be hit. Both present conditions and forward-looking signals look far from encouraging.

A macroeconomic cocktail

Still, bad news was once again interpreted as good news last month. In August, the Federal Reserve (FED) had already acknowledged the weakness in the labor market, so the negative surprise was small, if not negligible.

On the contrary, in the first two weeks of September, equity markets gained a few percent, and crypto benefitted as well. The combination of a deteriorating labor market and the absence of rising inflation makes accommodative Fed policy seem inevitable, an outlook investors have welcomed.

Cause and effect

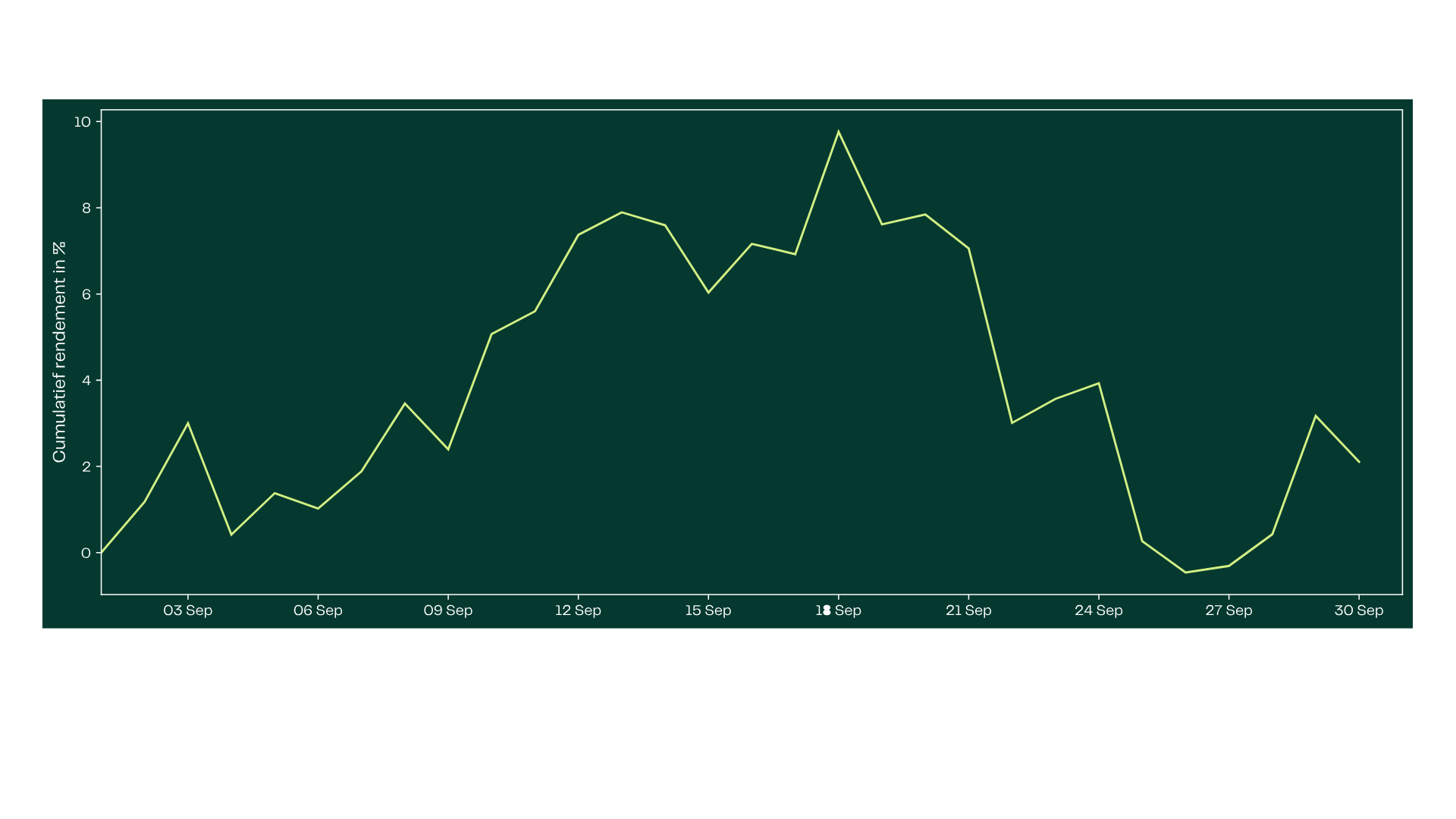

Despite the positive sentiment around the expected rate path, the party ended by mid-September. On September 18, the day after the Fed’s long-anticipated rate cut, the crypto market hit a local top. From there, the second half of the month turned red. Across the board, crypto lost more than 10%, with September 22 marking one of the largest liquidation waves of the year.

Figure 2: Cumulative return of the total crypto market, approximated by the MarketVector™ Digital Assets 100 Index

As is often the case, observers scrambled for an explanation after the fact. These are typically post-hoc analyses, yet still valuable because they highlight perceived causes that can contain useful information. And more often than not, the word “perceived” matters more here than the word “cause.”

This time, attention turned to the wave of liquidations: leveraged derivative positions closed out for lack of collateral. The implication was that too many investors were betting heavily on higher prices, pointing to an “overheated market.”

What is often overlooked, however, is that most centralized exchanges do not fully report liquidation data, given the technical complexity involved. At present, Bybit is the only major exchange to publish all of its liquidation data. Yet Bybit represents less than a quarter of the total market. On that basis alone, it is difficult to draw hard conclusions about the market’s overall state.

No euphoria, but a pattern

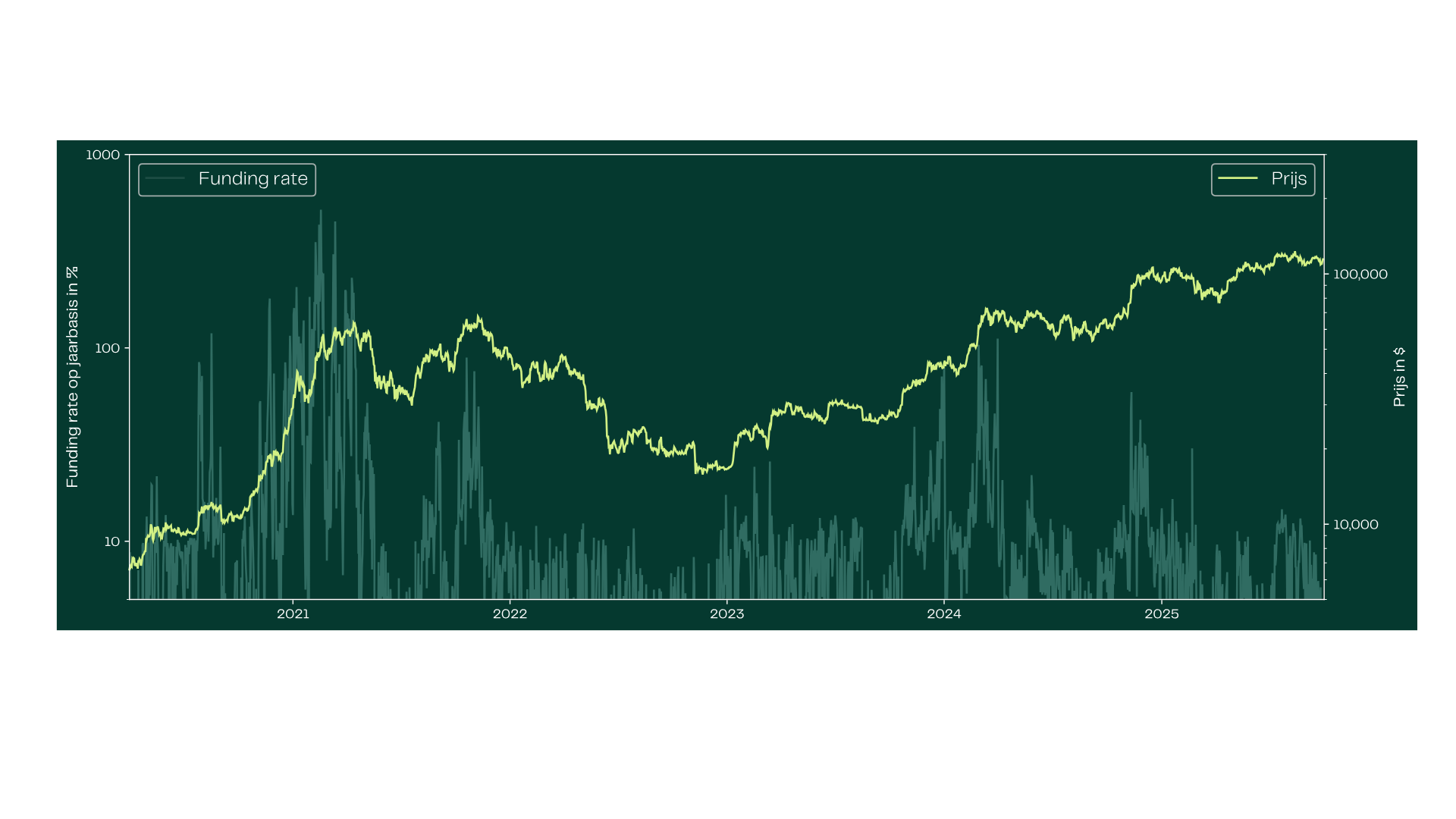

In our view, the market as a whole still shows little sign of overheating. The clearest evidence is the relatively low funding rate. This metric, from the same derivatives market as liquidations, reflects the extent to which traders are speculating on rising or falling prices. Historically, moments of euphoria, market tops and overheating have been marked by annualized funding rates in the tens or even hundreds of percent. Today, bitcoin’s rate sits only at a few percent, and for many altcoins it is even lower.

Figure 3: Annualized bitcoin funding rate (left) versus bitcoin price (right)

So if there is no overheating, why did the market turn lower after the rate cut? In our view, it was nothing more than a case of “buy the rumor, sell the news.” Prices fell simply because the main driver of earlier gains had already played out. With the next Fed decision scheduled for October 29, the same pattern could repeat, unless other developments take over to support positive sentiment.

What we will be watching in October

In the coming month, we will be watching closely for answers to the following:

- Will expectations of rate cuts help revive the U.S. labor market?

- Are we really seeing signs of overheating, or is there still room to run?

- Will the focus in October shift beyond macroeconomics?

Download the Monthly: September 2025

The PDF is available in Dutch only.

Our website uses cookies

We use cookies to personalize content and advertisements, to offer social media features and to analyze our website’s traffic. We’ll also share information about your usage with our partners for social media, advertising and analysis. These partners can combine this data with data you’ve already provided to them, or that they’ve collected based on your use of their services.