Monthly: May 2025

The market is feeling a bit chilly

5 June 2025

Summary

At first glance, easing inflation figures and some positive geopolitical signals suggest a calm summer for risk markets. However, beneath the surface, new inflation fears are brewing, and the U.S. economy appears far from recovered after recent turmoil. This climate breeds uncertainty—even in a bitcoin market that has climbed to new heights.

May 2025 will forever be remembered as the month bitcoin set a new all-time high. Or at least, we hope someone puts that in writing—otherwise, this milestone may fade into obscurity. Evidently, even something as objective as a record price isn’t enough to put the market center stage.

Changing of the currency guard?

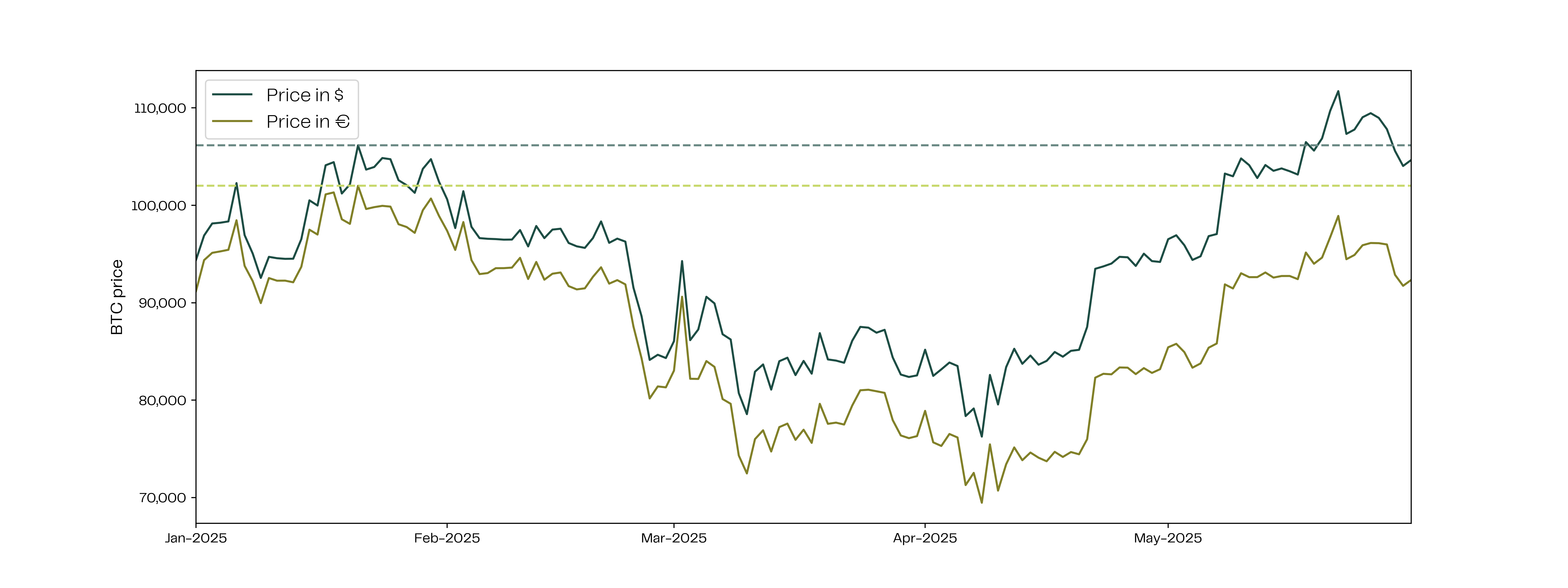

In the previous Amdax Monthly, we noted the weakening of the U.S. dollar, a trend increasingly evident under President Trump’s economic policies. This observation was reinforced this month—not due to the belated credit downgrade by Moody’s, but more so by ongoing weakness in bond and currency markets. The dollar hasn’t recovered from last month’s 5% decline against the euro.

It would be simplistic to suggest bitcoin is directly benefiting from this dollar weakness. Still, it’s worth noting that bitcoin’s new record was priced in dollars, not euros. Is that why the milestone drew little attention? Not quite. As long as only 0.2% of all stablecoins are euro-pegged, the euro remains irrelevant in the crypto power play.

Figure 1: Bitcoin price in USD and EUR, with pre-May highs marked by dotted lines

A cool spring

The crypto market isn’t exactly capturing the interest of new investors—something any analyst could tell you without hesitation. Major media, including the recognized Dutch newspaper FD, barely acknowledged the fresh all-time high. Coinbase’s App Store ranking hovered around 300, and search traffic for “bitcoin” has been trending downward since November.

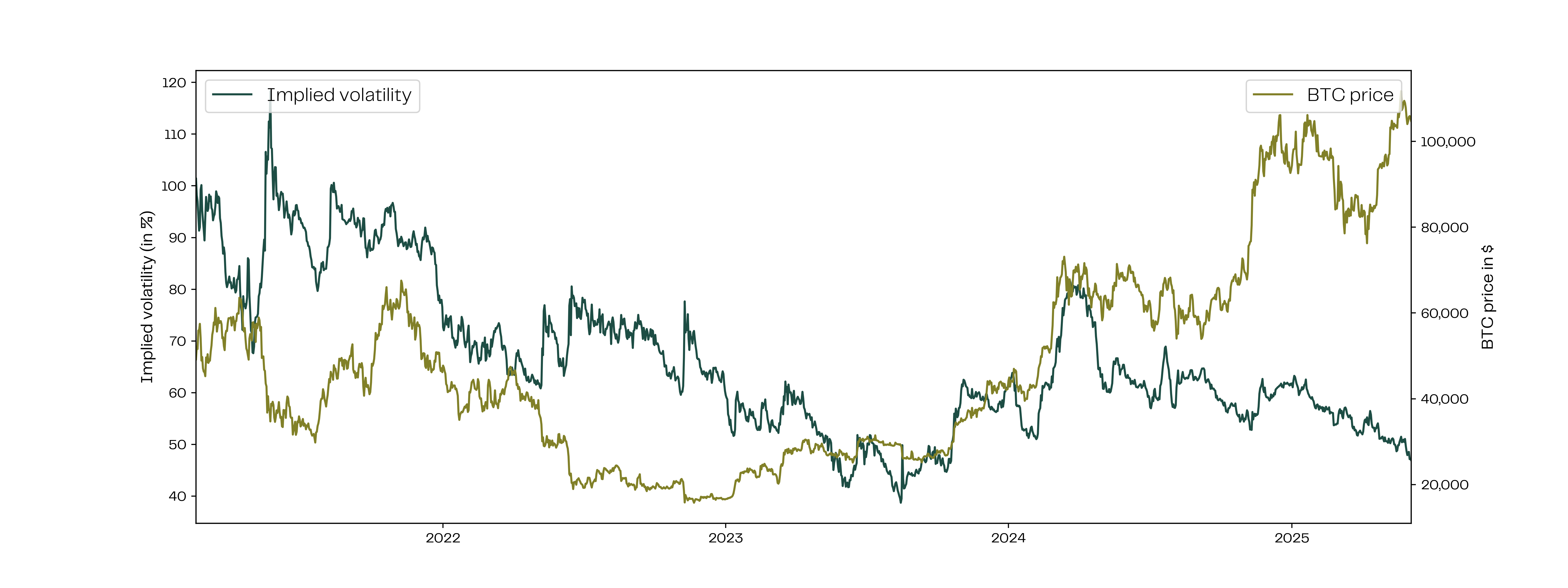

There’s also no sign of renewed risk appetite. Implied volatility—market expectations of price swings based on derivative pricing—has dropped to its lowest level in over 18 months.

Figure 2: Six-month implied volatility (left) vs. bitcoin price in USD (right)

Typically, this volatility increases during bull markets when speculative investors dominate. Now, derivatives markets suggest minimal risk in either direction. With bitcoin dominance above 60%, there’s no visible shift toward riskier altcoins. As asset managers, we’re always alert to the risk of overheating, but this market feels rather frosty.

Fears of a tepid summer

To understand the lack of risk appetite, we turn to macroeconomics. Despite ongoing tensions, the U.S. and China appear willing to negotiate, and fears of new EU tariffs lasted only two days. Additionally, both consumer and producer price indices came in lower than expected this month—meaning observable inflation is still absent. Historical data looks reassuring, but it doesn’t tell the full story…

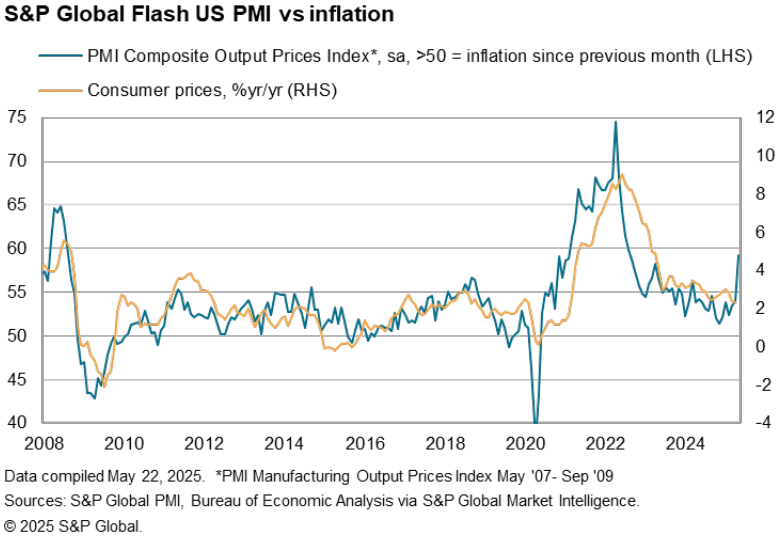

The Purchasing Managers’ Index (PMI) surveys business managers responsible for procurement, staffing, and inventory. While subjective, PMI is a historically reliable leading indicator for inflation. This month’s figures—impacted by tariff dynamics—pointed to declining employment and rising input costs, potentially signaling future inflationary pressure.

Figure 3: Reported input prices (left) vs. consumer inflation (right)

‘Hard’ data (measurable, backward-looking) continues to paint a strong economic picture. But ‘soft’ data (forward-looking expectations) tells a gloomier story. As a result, the Federal Reserve keeps pushing back its long-anticipated rate cuts. Where five cuts were once expected in 2025, only two remain on the table.

Equity markets appear to be climbing again, but not yet reaching new highs. As long as hard and soft data diverge, we find it unlikely that risk appetite will fully return—across both traditional and crypto markets.

Key themes to watch in the coming month

- Will bitcoin continue setting records in June, and this time spark actual euphoria?

- Will signs of a trade war fade, and geopolitical uncertainty under Trump ease?

- Will ‘hard’ and ‘soft’ macroeconomic data finally converge?

Download the Monthly: May 2025

The PDF is available in Dutch only.

Our website uses cookies

We use cookies to personalize content and advertisements, to offer social media features and to analyze our website’s traffic. We’ll also share information about your usage with our partners for social media, advertising and analysis. These partners can combine this data with data you’ve already provided to them, or that they’ve collected based on your use of their services.