"Negativity mainly comes from investors who had counted on an “Uptober” month."

2 October 2025

Monthly: October 2025

Summary

While early in the month people were still cheerfully pointing to the supposed correlation between precious metals and bitcoin, a sharp price drop hit many crypto investors like a cold shower. Bitcoin turned out not to be a safe haven after all, but subject, among other things, to the turmoil around the U.S. government and global unrest caused by Chinese export restrictions. The sour mood, however, seemed largely confined to the group of investors who may have been a bit too optimistic.

“Noble metals and cryptos to peak as confidence in currencies wanes,” headlined Het Financieele Dagblad on October 7th. It feels like months since bitcoin was still printing all-time highs. In a way, it is reassuring that fewer than four weeks have passed since the current price record of roughly $126,000 was set, but perhaps that sense of defeat is the real problem…

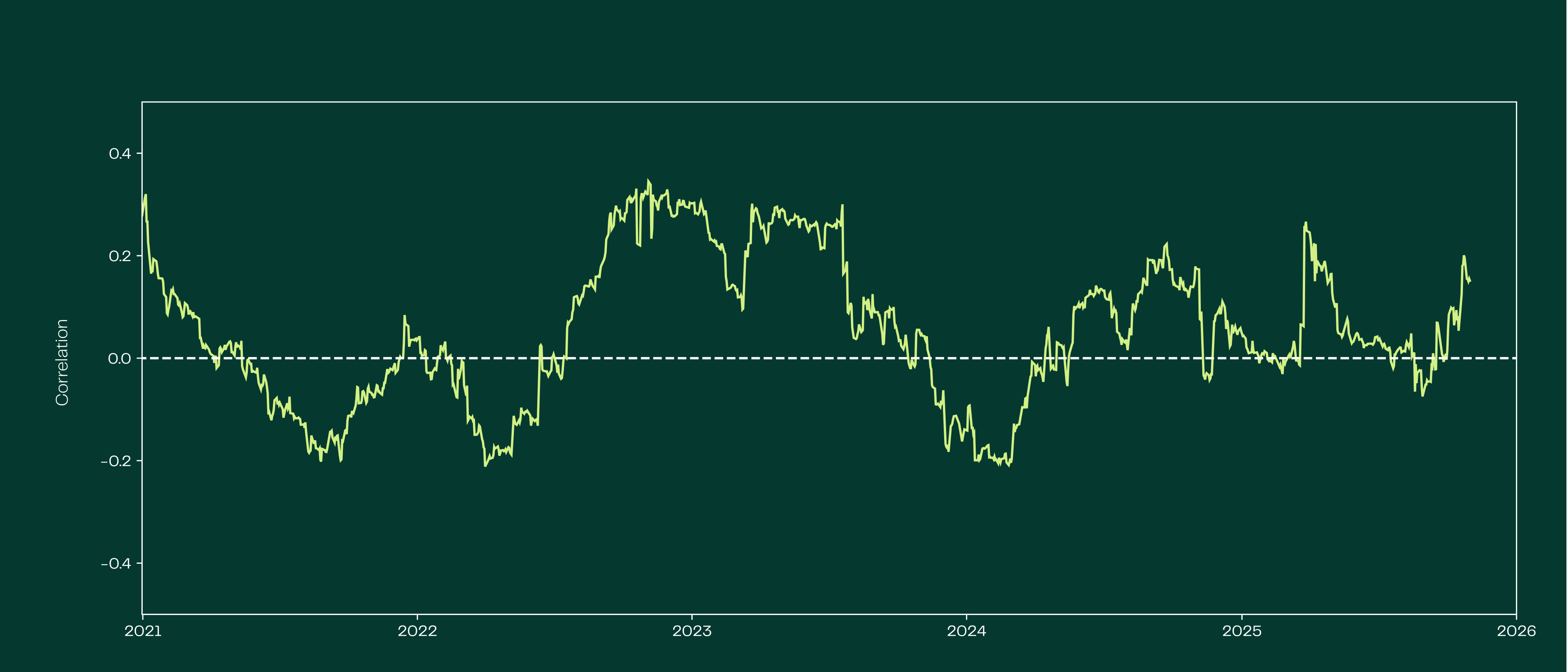

Correlation illusion between gold & bitcoin

The article attributed the dizzying price moves to the decline of the U.S. dollar and a lack of confidence among investors. In that line of reasoning, crypto was implicitly cast as a safe haven, something many crypto investors had previously only dreamed of.

It remained a dream. While gold and silver continued their surge, crypto was dealt a harsh blow days later as roughly $800 billion in value evaporated. No safe haven, but a volatile, high-risk asset.

We were surprised as to where the FD got the idea that bitcoin behaves like precious metals. Yes, they rose for a brief period, but the correlation between bitcoin and gold has hovered fairly steadily around zero for years. A closer look at the data leaves far less room for illusion.

Figure 1: The 90-day correlation between the bitcoin and gold price since early 2021

The strength of bitcoin

There is nothing inherently wrong with concluding that crypto remains a high-risk asset class. In fact, this characteristic represents the very foundation of its strength and long-term growth potential. Historically, volatility in the crypto market tends to peak during periods of significant price appreciation, the largest movements typically occur on the upside.

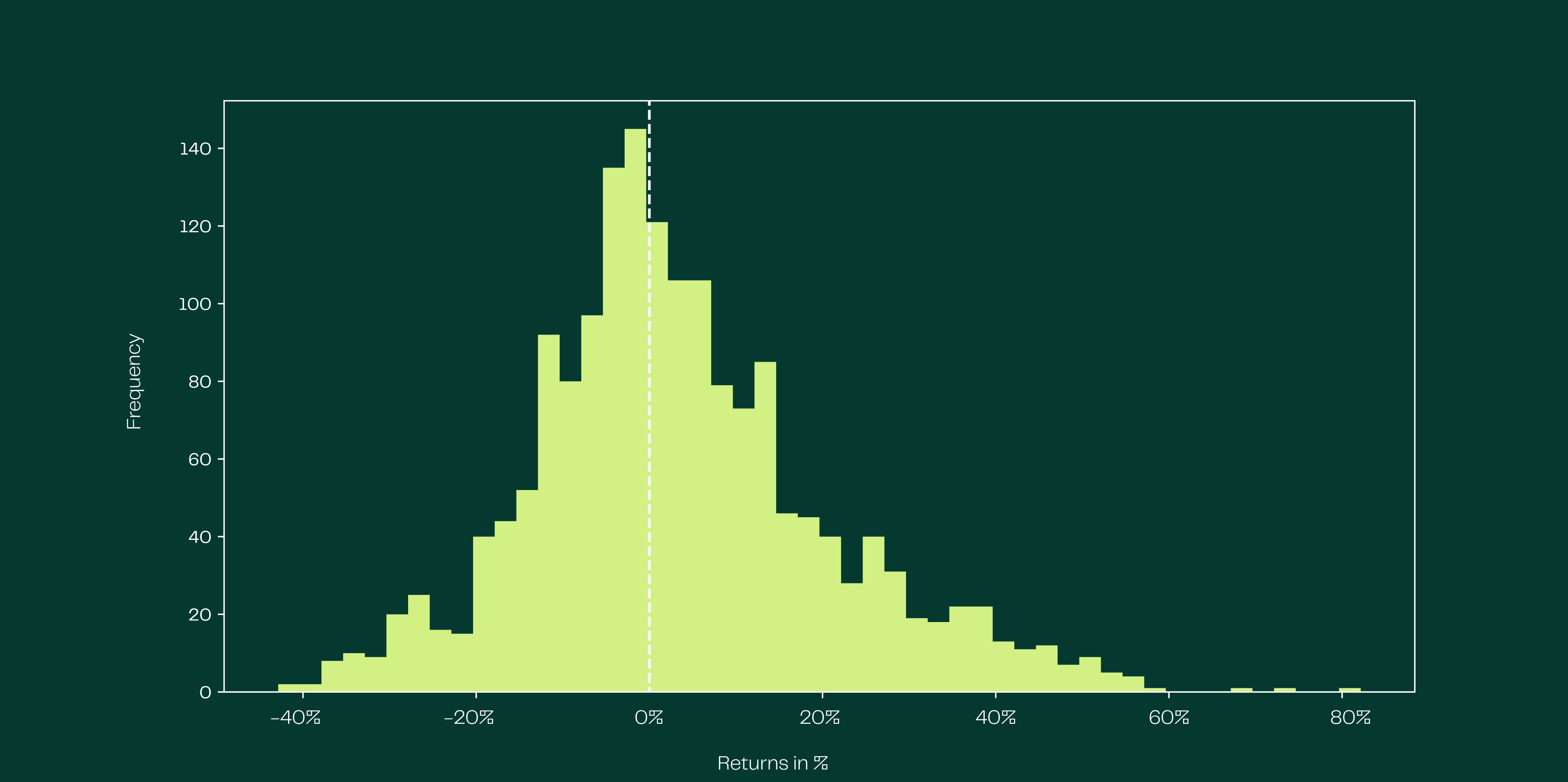

The histogram below illustrates that 30-day returns exceeding +40% occur considerably more often than declines greater than -40%. This asymmetry makes bitcoin an attractive addition to a diversified portfolio, even though modest price dips (ranging from -5% to -1%) are most frequent. In statistical terms, this phenomenon is referred to as positive skewness. For quantitatively inclined investors, it is a compelling reason to include crypto assets within a multi-asset investment strategy.

Figure 2: A histogram of 30-day bitcoin returns since early 2021

The traditional investor group certainly cannot be blamed for last month’s developments. Although the bitcoin price declined by -3.9% and ether fell even further by -7.2%, roughly $4 billion in new capital flowed into spot ETFs.

This suggests that the prevailing negativity mainly stems from investors who had been counting on a spectacular “Uptober” month.

That notion offers a certain level of reassurance. The negative sentiment appears to be concentrated among a group of investors who tend to change their outlook as soon as the price moves in the opposite direction. In our view, that does not constitute structural negativity.

As is often the case, explanations soon follow to rationalize the observed price movements, typically a case of hindsight analysis, but no less valuable, as these reflections often reveal useful insights into the perceived causes behind market developments. And more often than not, the term perceived proves to be far more relevant than the term cause.

A month without economic data

October will also go down in history as the month without a U.S. government. Due to the so-called government shutdown, a significant portion of federal employees were furloughed throughout the month. For financial markets, this meant that little to no macroeconomic data was released.

The Federal Reserve (Fed) was not deterred, lowering interest rates, as expected, by 0.25%. However, this did not lead to a relief rally in the markets. Fed Chair Jerome Powell emphasized that another rate cut in December is far from a “done deal,” thereby flattening the projected interest rate path considerably.

The lack of data has, in a sense, made it easier to address the questions we posed last month. Will rate cuts help revive the U.S. labor market? We simply do not know. Did the focus in October shift away from pure macroeconomics? Absolutely.

The ongoing trade war

China decided to pour more fuel on the fire of the trade war by tightening its export controls. Under the new measures, the Chinese government must grant approval for all trade involving products that contain rare earth elements originating from China. This sudden assertion of control over international trade did not sit well with the White House, which immediately responded with threats of steep import tariffs.

This marks a new chapter in the ongoing trade war, one that continues to capture the attention of global financial markets. In the short term, the situation appears to have limited impact, but long-term, the dynamics between the two superpowers could contribute to renewed inflationary pressure. In that case, we might even find ourselves hoping that the government shutdown continues. After all, if you stop publishing the data, the problem does not officially exist. Right?

What we will be looking out for in November

In the coming month, we will be watching closely for answers to the following:

- Are crypto investors losing faith in a positive final quarter?

- Are we missing key macroeconomic developments due to the government shutdown?

- Will the effects of the reignited trade war start to be felt across markets?

Download the Monthly: October 2025

The PDF is available in Dutch only.

Our website uses cookies

We use cookies to personalize content and advertisements, to offer social media features and to analyze our website’s traffic. We’ll also share information about your usage with our partners for social media, advertising and analysis. These partners can combine this data with data you’ve already provided to them, or that they’ve collected based on your use of their services.